Here at Storycase we’ve been involved in digital transformation programmes for both the private and public sector. Working with several of industry’s best architects and designers we understand what’s needed to deliver a service that meets the customer’s needs without costing the earth.

With this lens we’re posting a series of articles to highlight failings we’ve found while using digital services. The intention is to name and shame – not maliciously but to put pressure on organisations to change the way they operate – and to deliver services that work.

As bank and building society branches close we’ve come to rely on online services and mobile apps for our daily financial transactions. When these do not work as expected we justifiably get annoyed and the stress levels in our daily lives are raised. So what went wrong at YBS when trying to open a joint account and what lessons can we learn?

Yorkshire Building Society – YBS Joint Account Opening Problems

As mentioned in our previous post Yorkshire Building Society Design Failings – with increasing inflation rate here in the UK, like many customers with some cash savings we need to open a new YBS account to get a better interest rate. YBS fail to pass on bank base rate increases to existing savers while immediately hiking mortgage rates. Building societies create new account variants that pay a higher interest and fail to pass on rate hikes on older accounts penalising existing customers who fail to act.

So after less than a year of opening an account we must apply for a new account to chase top rates. It sounds easy – just apply online today! No it’s not that easy at all and here’s why.

The use case we need is to open a joint account and that’s not been considered a minimum viable product by YBS. While the online form does indeed provide a joint account option, selecting it takes the user down a rabbit hole.

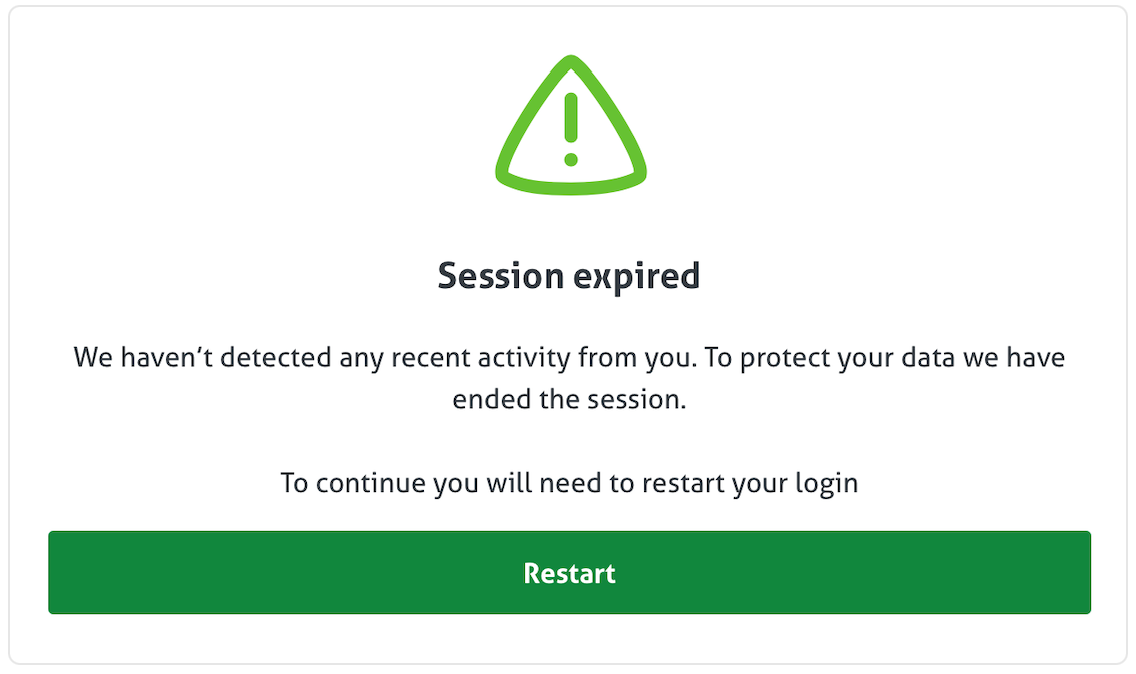

The form blindly asks for the full details of the joint account holder including a password but does not explain why. And entering all these superfluous details takes time that’s not been allowed so the online session can time out when the customer clicks submit.

Adding a simple question – Does the joint account holder already have an online account? and if so entry of a username would avoid confusion. But no, the first account holder – they must have an online account in order to apply – is forced to type in the joint holder’s full name, phone numbers, email addresses and passwords that are all unnecessary and so infringe GDPR.

Bad service design

Of course the simplest way for existing joint account holders to open a new variant of an existing account eg from a Saver Plus Issue 12 to Saver Plus Issue 13 is to offer an upgrade on the existing account. This enables all account holder to be pre-filled but would be too easy and defeats the real object in YBS creating the new issue in the first place.

Faced with YBS’s joint account opening form the customer has two options. Neither are good. The first option is to enter the second account holders details including passwords to match the online account that already exists. The second is to give up with opening a joint account and apply to add a second account holder later – which can only be done via post.

If the second account holder does not have an online account the current form makes more sense but the password should only be set up by the second user at first login to avoid security issues.

Adding a second account holder is not an online option even for an online only savings account so a paper form must be posted out and returned. With severe postal delays due to Royal Mail strikes and staff shortages here in the UK customers want to avoid post.

Both journeys will time out if the user does not enter all the information within an unspecified time period or the session will timeout without warning. Clearly no user research or UX has shaped these journeys – I wonder why?

Clearly it is not in YBS’s financial interest to improve the account opening journey for existing savers – it’s why they created the new account variant in the first place. We complained about the joint account opening experience when it happened a year ago and nothing’s been done. The user journey is still broken.

Can it get any worse?

Well, yes it can. After calling YBS customer services and being advised to clear cookies or try another browser and try again (we did neither) we persisted with the joint account user journey.

Initially it looked successful – the account was opened with an email to both account holders. But the joint account was not visible to the second account holder despite the registration email stating it would be activated overnight.

It took a further phone call to learn that YBS systems can take up to ten days to merge details and a temporary customer number would be posted out in the meantime. No mention of this online or in the email. Again, the user journey has not been considered.

Design Failing Summary

- Account opening form times out without warning – all data entered is lost and customer has to restart the journey.

- Joint account holder credentials – first applicant forced to enter second account holder’s password

- No option to use an existing joint account details to open a new account – this would avoid needless data entry.

Come on YBS – fix your poor online service design or better still, stop the bad practice of spawning new account variants to penalise existing savers.